Otvoriť spoľahlivú miestnu peňaženku pred cestami. Zadaním údajov raz vytvoríte dlhý, spoľahlivý kanál pre nákupy; používajte ho na dopravu, potraviny, ubytovanie; uchovávať zálohu v fyzických poznámkach na prípad núdze; skontrolujte odkaz pre podrobnosti z oficiálnych irena smernic.

Uprednostňujte platby na základe plastových karet, ak je to možné. Odkaz na váš primárny zdroj financovania zabezpečuje rýchle doplnenie; ak je obmedzené pripojenie, režim offline umožňuje transakcie; držte malú sumu fyzických bankoviek ako záložu pre trhy; taxíky; predajcov na ulici.

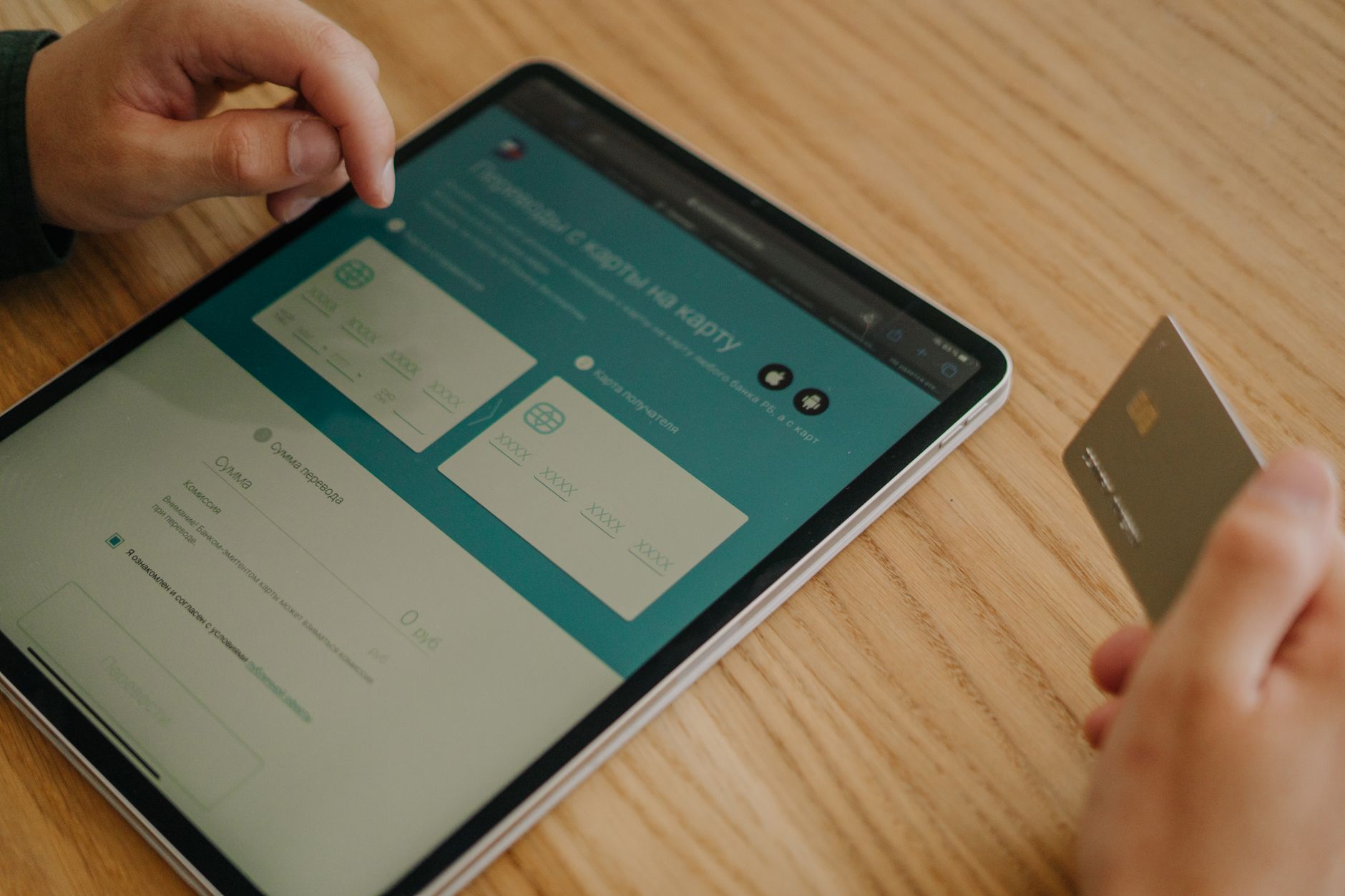

Prevod peňazí zo zahraničia vykonajte cez MoneyGram alebo Azimo. Cestovné vyžadujú rýchle doplnenie; cudzinci z toho majú výhodu; prevody sa dokončujú s nízkymi poplatkami; uveďte meno príjemcu a údaje o peňaženke; oficiálne náklady a časové rámy zistite cez odkaz poskytovateľa.

V Európe široko podporujú obchodné siete platby cez peněžné peňaženky; dôvody sú pohodlie; to vysvetľuje, či obchodníci prijímajú dotyky, kódy alebo skenovanie. Odkaz na oficiálnu FAQ vysvetľuje limity a výnimky.

Dokončené bezpečnostné kontroly znižujú riziko; PIN kódy sa zadávajú len na spoľahlivých zariadeniach; sledujte kurzové lístky na kioskoch; udržiavajte záložný plán počas dlhých ciest; povinné kroky pre dodržiavanie predpisov musí byť dodržiavané; tento prístup pomáha cudzincom vyhýbať sa prekvapeniam.

Platobný krajina v Rusku 2025

Začnite zmiešanou železničnou stratégiou: dajte prednosť reálnym prepravám cez stanovené siete; držte niektoré prostriedky v likvidných miestnych účtoch; potom rozširujte.

Osídľovanie sa smeruje k mobilným peňaženkám; okamžité platobné systémy zachytávajú väčšinu; fyzické peniaze zostávajú v regionálnych trhoch. Avšak kľúčové platobné systémy zahŕňajú platformy Unicredit; koridory Moneygram spájajú regióny; okruhy Yianpay podporujú prieskumné prehrady; tieto poskytujú alternatívy k tradičným plastovým platobným nástrojom.

Onboarding pre prienčných tokov zákazníkov sa spolieha na robustnú KYC; jednotlivý riaditeľ z regionálnej banky uvádza imigračné kontroly ako podstatné; plán pracuje s multikanálovou verifikáciou; rýchle express prevody.

Romské analytiky ukazujú, že dlhšie migračné cykly ovplyvňujú likviditu remesií; imigračné relácie vytvárajú ťažkosti; pilotné projekty v Malajzii ukazujú rýchlejší prienos cez digitálne trate. Integácia s Apple zlepšuje prihlásenie; náhodné použitie zariadení vyžaduje zvýšenú bezpečnosť; kódy dodávané cez OTP zabezpečujú správnosť.

Používanie hotovosti v Rusku: kde vybrať ruble a tipy pre bankomaty

prvé, čo robiť: otvorte si lokálnu peňaženku na významnej sieti; overte si kompatibilitu so svojou domovskou bankou pred cestovaním; noste s sebou záložnú bankovú kartu; udržiavajte malú sumu peňazí na bezpečnom mieste pre prípad núdze.

Hľadajte bankomaty v bankových pobočkách; prehľadávajte obrazovky s pokynmi; nachádzajú sa v centrách miest; letiskách; univerzitných kampusoch; tieto stroje obvykle zobrazujú jasnejšie informácie o poplatkoch; vyhýbajte sa strojom s opotrebovanými klávesnicami; dbať na možnosti jazyka; ak vás požadujú dynamickú konverziu meny, odmietnite DCC.

denné limity sa líšia; typické rozsahy: 5 000 až 60 000 miestnych jednotiek za deň na kartu; skontrolujte každú inštitúciu; poplatky sa líšia podľa vydávajúceho; rozvrhy poplatkov sa zobrazia na obrazovke; vyberte možnosť s najnižšími poplatkami; Okrem toho niektoré banky uvalia poplatky za používanie v zahraničí; dajte pozor na skutočnú cenu výberov.

Sanácie núkajú cestujúcich hľadať alternatívy; výbery cez MIR fungujú na mnohých miestach; partneři podporujú medzinárodné sieťe; čo robiť, ak je prístup zastavený: mať pri sebe miestnu menu; pri skúmaní iných metód môžu pomôcť možnosti peňaženiek, ako sú predplatené peňaženky; kryptomeny môžu slúžiť ako finančný mostík pre cestovné potreby; izvestiaeduard povedal, že tento prístup sa stal častejší pri strihších režimoch.

V prípade cestovania je dôležité zistiť si lokálne informácie; prehľadávať univerzitné bulletiny; krajiny s uvoľnenými obmedzeniami často publikujú tipy pre cestovateľov; dbať na bezpečnosť a ochranu osobných údajov; porovnávať možnosti pred cestou; vybrať metódu najlepšie vhodnú pre účely ako štúdium, práca alebo rekreácia.

Akceptácia kariet v Rusku: Visa, Mastercard, Mir a miestne sieťe

Nesete Visa, Mastercard vydané významnou bankou; Mir slúži ako spoľahlivý záložný variant. Mestské terminály hlásia vysokú pokrytnosť: prijímanie Visa okolo 95-98 percent; Mastercard podobne; prítomnosť Mir v veľkých centrách sa odhaduje na 80-90 percent. Terminály Mir prijímajú platby v týchto centrách; možnosti mobilného tapu zvyšujú bezkontaktné platby na všetkých platobných miestach.

Geografická pokrytnosť sa líši podľa lokality. Centrálne huby, ako je hlavné mesto, ukazujú takmer univerzálnu podporu pre tri siete; provinciálne mestá majú mezeru v obchodoch na vidieku; mnohí malí obchodníci sa stále spoliehajú na fyzické peniaze alebo domáce platformy.

Domestická platforma sa rozširuje, keď sa niektoré inštitúcie pripojia k schémam založeným na Miro; NSPK, kľúčová inštitúcia založená na spracovaní transakcií Miro, zabezpečuje hladký účetný výstup po celom štáte. Niektoré regionálne banky vydávajú plastové karty spojené s Miro; okrem sieťových značiek v minulosti boli obdobia obmedzenej zahraničnej akceptácie v dôsledku sankcií; teraz pokračuje obnovenie. Cudzí návštevníci z Ameriky alebo Veľkej Británie typicky vidia, že Visa a Mastercard sú prijímané v letiskách, hoteloch a veľkých obchodných reťazcoch. Miro zostáva prijímané vo väčšine domácej sieťou.

Výmenný kurz: obchodníci môžu ponúkať dynamickú konverziu meny; aby sa minimalizovali náklady, konvertujte na platforme vydávajúcej platobnú kartu pred platbou; používanie cudzieho plastu môže mať vyššiu maržu výmenného kurzu; sledujte sumu na účetnici, aby ste potvrdili zhodu s oficiálnym kurzom; v praxi väčšina terminálov používa domáce kurzy, nie medzinárodné; niektoré terminály zobrazujú označenie kurzu; hľadajte logo miestnej banky, aby ste potvrdili úhradu.

Praktické kroky pre cestujúcich: overte si medzinárodné použitie s vydávajúcou bankou; uistite sa, že sú povolené mobilné peňaženky alebo bezkontaktné platby; povolte upozornenia cez Twitter od vydávajúceho subjektu na výpadky; plánujte záložný variant pomocou fyzických peňazí ako zálohy, aj keď sa chcete spoliehať na plastové karty; poslednú chvíľu zmeny plánu vyžadujú rýchlu adaptáciu; držte malú sumu fiat peňazí pripravenú pre miesta, kde nie je prijatá elektronická platba; skenujte QR kód, ak to podporuje obchodník; tato metóda funguje s Mir alebo cross-brand platformami; hľadajte logá, aby ste potvrdili kompatibilitu; zdieľajte informácie so svojou hostiteľskou inštitúciou pred príchodom.

Pozrite sa na budúce pokrytie: na hlavných dopravných uzloch táto platforma funguje hladko; akceptácia rastie, ako sa banky pripojujú k spoločným koľajom; jednotlivci plánujúci cestovanie by mali pripojiť sa k plánu sledovať domácu trhové posuny cez twitter vydavateľa; niektoré inštitúcie predtým prevádzali samostatné sieť; teraz sú zjednotené do jediného systému; dlhodobý plán preferuje Mir pre domácu spotrebu, zatiaľ čo Visa a Mastercard si udržiavajú široký dosah v zahraničí; krokom za krokom, overte si možnosti pred príchodom; potvrďte si to s hostiteľským miestom; dokončte transakciu skenovaním alebo dotykom.

Mir v zahraničí: ktoré krajiny prijímajú karty Mir a ako ich používať

Pred cestou sa uistite u svojho vydávateľa, napríklad Tinkoff, či Mir funguje v destinácii; ak sa dohodli, otvorte medzinárodný plán používania; skontrolujte poplatky za výbery; zistite denné limity; uchovávajte kontaktné údaje zákazníckej podpory na prípad núdze.

Globálne pokrytie je najsilnejšie v krajinách SNS; rastie aj v susedných trhoch; v niektorých prípadoch bolo použitie Miru dočasne zastavené; pri dlhých pobytoch môžu vzniknúť otázky imigračného charakteru; ak sa presúvate, kontaktujte vydávajúceho subjektu včas; zdieľajte tieto rady s rodinnými príslušníkmi, ktorí vás sprevádzajú.

- Kazachstan

- Kirgizsko

- Belarus

- Armenia

- Uzbekistan

- Türkiye

Používateľská príručka: 1. Vyhľadávanie - Použite vyhľadávacie pole na hornom okraji obrazovky. - Stlačte kláves Enter alebo kliknite na Hľadať. 2. Filtrovanie - Vyberte kategóriu z rozbaľovacieho zoznamu. - Použite filtre na pravom okraji, aby ste zúžili výsledky. 3. Zobrazenie - Pre prehliadanie v tabuľke kliknite na Tabuľka. - Pre zobrazenie na mape kliknite na Mapa. 4. Export - Stlačte Exportovať na dolnom okraji obrazovky. - Vyberte formát (PDF, CSV, Excel). 5. Nápoveda - Pre ďalšiu pomoc kliknite na Nápoveda v pravom hornom rohu. 6. Kontakty - Ak potrebujete podporu, kontaktujte nás na support@example.com alebo +1 234 567 890. Ceny a dostupnosť sa môžu meniť.

- Overte si logá pri ATM; MIR môže byť vedľa miestnych sieťov; ak je podporovaný, pokračujte s výberom alebo platbou; inak použite miestnu partnerku peňaženku alebo prevody cez Skrill.

- Čip s PIN kódom je typický; bezkontaktná platba sa môže objaviť; udržiavajte disciplínu pri používaní karty pre bezpečnosť.

- Provízie sa líšia; väčšina prípadov spracúvaných cez partnerské banky; skontrolujte aplikáciu vydávajúcej banky pre aktuálne poplatky.

- Keď priame platby zlyhajú, umožňujú usadenie prevody cez Skrill alebo podobné globálne služby; uistite sa, že prevody dodržiavajú miestne limity.

- Pre imigračné účely kontaktujte medzinárodnú službu vydávajúceho orgánu; Kornienko, riaditeľ partnerskej banky, uvádza možné výnimky; preto zdieľanie cestovných plánov so zákazníckou podporou pomáha vyhnúť sa zastaveniam.

Digitálne peňaženky a bezkontaktné platby: aplikácie, ktoré fungujú v Rusku

Nainštalujte Google Wallet; pripojte svoju hlavnú kartu; povolte bezkontaktnú platbu na NFC termináloch v hlavných obchodných reťazciach.

Cestujúcim by mala byť pripravená stiahnuteľná elektronická peňaženka pred cestou; kontrola na imigračných úradoch zriedka blokuje tieto nástroje; uchovávať záložnú kartu ako predopatrnosť; aj pre ne-digitálne zvyklých, nastaviť bezpečnú hranicu; potom si vycvičiť s malou nákupom, aby ste vedeli, ako reaguje rozhranie.

Volet rozhrania, nazývané viacjazyčné peňaženky, zobrazujú štítky; vyberte osobné nastavenia; poznajte svoje limity; vrátane bezpečnostných upozornení; potom povolte odomknutie pomocou biometrickej autentifikácie pre rýchlosť a bezpečnosť.

Prechádzanie hranicami môže zahrňovať služby ako yianpay spojené s peňaženkami; izvestiaeduard poznamenal, že kancelárie veľkých bánk doteraz vyžadovali extra overenie pre nové zariadenia; ponuky sa líšia podľa vydavateľa; overenie môže byť dokončené cez mobilnú aplikáciu; potom sa staneš plynulým v miestnych mobilných platbách.

Vyberte si medzi možnosťami iOS alebo Android; musíte potvrdiť podporu vydavateľa; aplikácie sú k dispozícii na stiahnutie z oficiálnych obchodov; musíte overiť limity prevodov; Payoneer môže zúčastniť sa na prevodoch výnosov; môžete poslať žiadosť o platbu osobu cez QR kód; prekladateľ môže vám pomôcť počas cesty; cestovatelia z Hongkongu môžu tieto nástroje tiež používať; univerzitné výmeny sa na nich spoliehajú; uistite sa, že vaše osobné zariadenie udržiava vaše informácie v bezpečí; súhlasili ste s podmienkami o spojení.

| App | Kde to funguje | Notes |

|---|---|---|

| Google Wallet | Viac NFC terminálov | Široká podpora vydavateľov |

| Apple Wallet | iOS zariadenia s NFC | Vyžaduje kompatibilné vydavateľské spoločnosti |

| Samsung Wallet | Samsung zariadenia | Skontrolujte kompatibilitu vydávajúceho subjektu |

| volet | Rozhranie v niektorých prostrediach | Použite funkcie na navigáciu; overte kompatibilitu |

| yianpay | Prevody cez hranice | Prepojené na peňaženky; potvrďte dostupnosť s bankou |

Poplatky, obmedzenia a pasti s menami: ako minimalizovať náklady

Otevrite si lokálny bankový produkt cez platformu Sberbank pomocou online formulára; vyberte účet bez FX marže a uskutočňujte transakcie v skutočnej miestnej mene (RUB), čo minimalizuje riziko menovej konverzie. Vždy odmietnite dynamickú menovú konverziu na termináli alebo pri online platbe; takto si zachováte skutočnú kurzovú sadzbu vydávajúcej banky a ušetríte si na konverziách.

Poplatky, obmedzenia a riziká menovej politiky: ktoré náklady sledujte vrátane FX marží, nadprímernej marže obchodníkov a poplatkov za výbery na termináloch. Keďže mnohé sieťové operácie sú blokované pre niektoré medzinárodné transakcie, cestujúci, ktorí potrebujú využívať služby v rôznych krajinách, by mali sa informovať o medzinárodných limitách; tri najspoľahlivejšie spôsoby sú terminály v rámci siete, online bankové prevody a medzinárodné platobné platformy. Držte sa otvorených limitov, aby ste neplatili nadpoplatky.

Pasti pri menách: vyhýbajte sa obchodníckym konverziám; trvať na úhrade v rublech, aby ste dostali skutočnú medzibankovú sadzbu. Ak uvidíte výpis v inej mene, používajte miestnu možnosť a pozor na základné body a časové razítka uvedené v online formulári; písomné podmienky môžu skrývať marže, tak ich prečítajte pred potvrdením. Akceptácia sieťou ako American Express sa líši podľa krajiny a ikony terminálu; v niektorých miestach sú k dispozícii expresné možnosti.

Tri konkrétne kroky na minimalizáciu nákladov: najprv sa informujte o zníženiach poplatkov a denných limitách pred cestou; potom pripojte jeden účet na platforme, ktorej dôverujete; tretie, overte podporu terminálov v európskych sieťach a skontrolujte, či služba, ktorú používate, je v cílovom štáte otvorená alebo blokovaná. Ak sa vyskytne problém, okamžite kontaktujte podporu; poznajte, ktoré sieťe fungujú, ktorí obchodníci prijímajú daný nástroj a ako uchovať peniaze v bezpečí. Alexej zo Sberbanku zdôrazňuje, že vedenie záznamov v reálnom čase znižuje riziko a ušetri peniaze.